The gold and silver prices have since 2015 been in a secular bullmarket. Since the structural dip to test the trend in mid-2022, the two precious metals have seen a parabolic trend. This trend has only recently been broken. Q1 saw gold peak around $5600/oz and silver around $120/oz.

Secular bullmarkets go through regular re-tests. We’ve seen this both in the 2000-2010, as well as in the 1970’s bullmarkets.

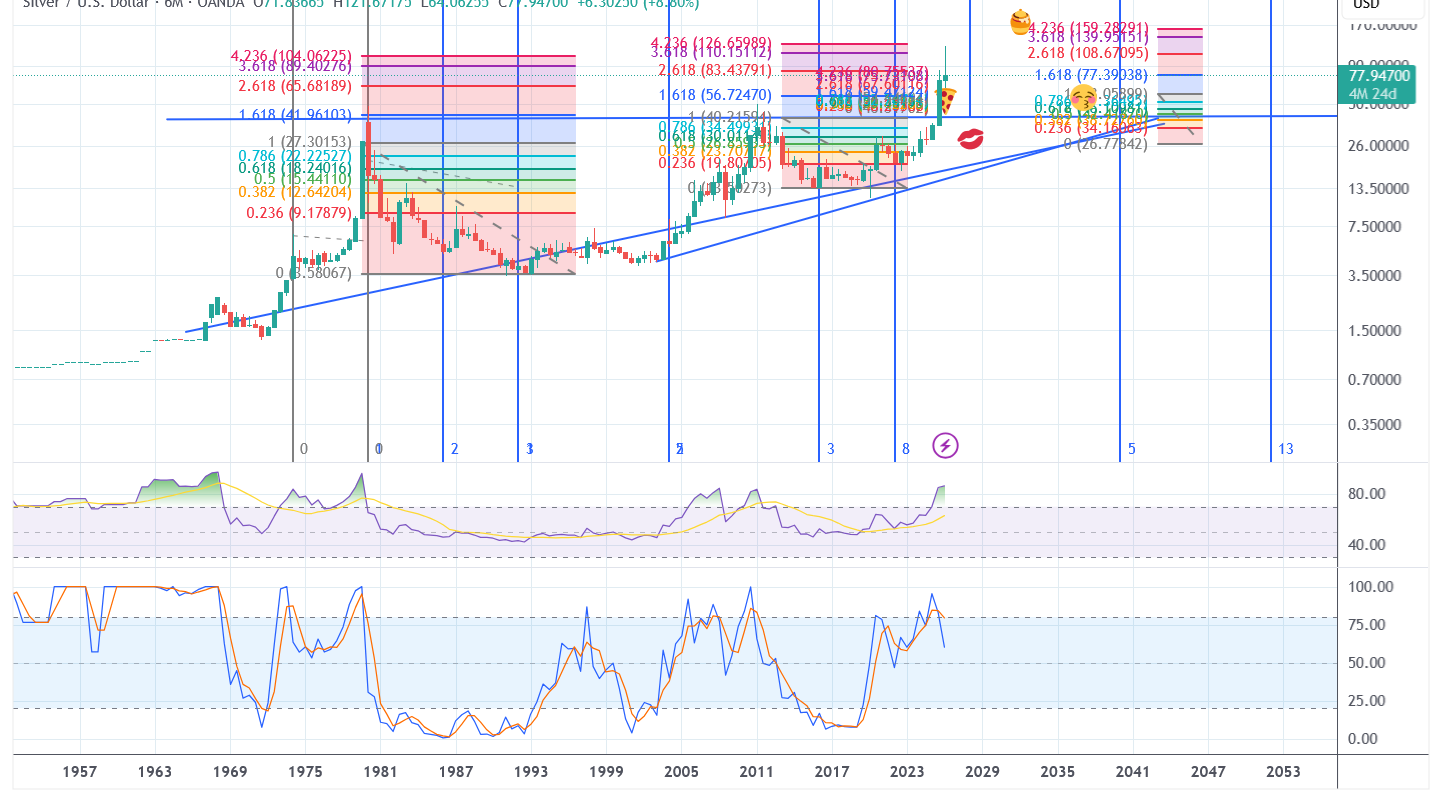

The silver market in particular has been a textbook example of a typical secular precious metals bullmarket.

Silver acts like an exaggerated gold with higher peaks and deeper valleys. The exhaustion candle on the silver’s 6 monthly chart therefore tells a story about an intermediate peak with a re-test around $30-40, the previous peak, before heading higher to complete the measured move around $200 to $300/oz. This would happen as a cyclical peak, coinciding with a broader bearmarket in equities and an energy sector bullmarket.

Miners run twice, following the Lassonde curve

Pierre Lassonde illustrated his famous curve of a resource stock, where a mining equity first runs on the value of the deposit and secondly on the value of the mine with a valley between the two. The curve would express itself on the risk curve from the least risky to the most risky. The majors would run first, then the juniors, then the developers, then the explorers and then the liar with a hole in the ground. Silver miners follow the pattern almost to the tee. As we wrap up the interemediate peak and the dip that follows, we may see silver miners phenomenally catch up with the metal prices, as we already have witnessed in the already concluded season.

Notwithstanding, in addition to the silver miners, also gold, copper, lithium, graphite, uranium and strategic industry minerals stand to benefit from the upcoming season. The sweet spot stands where rarity meets demand.